Buying a dental practice can open the door to ownership, but the financials need to support the purchase before you move forward.

For many dental practice acquisitions, SBA 7(a) financing may be an option, depending on the borrower, practice, transaction structure, and lender underwriting.

A dental practice may look healthy on the surface: steady patient flow, modern equipment, a recognizable name in the community, and a seller who is ready to transition. But before you commit to a purchase price, financing structure, or letter of intent, it is important to understand what the financials are really telling you.

In this article we are going to look at 10 numbers that deserve careful review before buying a dental practice.

1. Gross Revenue

Gross revenue is easy to like and easy to misread.

A dental practice may show strong collections, but the better question is how durable those collections are after the seller leaves. Look beyond the top-line number and study where the revenue is coming from. Is it supported by routine hygiene and recurring patient relationships, or is it being lifted by one-time restorative cases, implant work, cosmetic procedures, or a particularly productive seller?

It is also worth separating revenue by provider and procedure category. If the selling dentist is responsible for most of the high-value production, the buyer needs to understand how much of that revenue is likely to transfer. A practice that depends heavily on the seller’s personal clinical style, referral relationships, or treatment planning philosophy may carry more transition risk than the gross revenue suggests.

Pay attention to timing, too. A revenue spike may reflect pent-up demand, expanded hours, a temporary associate, aggressive treatment planning, or a short-term marketing push. Those numbers may still be valid, but they should not automatically be treated as the new baseline.

One of the most useful comparisons is production versus collections but take it a step further: look at collection percentage by payer type, procedure mix, and aging category. A practice can produce well and still collect unevenly if insurance follow-up is weak, patient financing is inconsistent, or older balances are being carried longer than they should be.

For a buyer, the goal is not just to confirm that the practice has revenue. It is to understand how much of that revenue is repeatable, transferable, and strong enough to support the purchase price, operating costs, owner compensation, and proposed debt service.

2. Seller’s Discretionary Earnings

SDE is where a lot of dental practice deals start to get fuzzy.

On paper, Seller’s Discretionary Earnings (SDE) is supposed to show the cash flow available to one full-time owner-operator before debt service. In practice, it can become one of the most negotiated numbers in the deal, because it depends heavily on what gets added back, what gets normalized, and what expenses will continue after closing.

The key is to separate cash flow that truly transfers to you from cash flow that only existed because of how the seller ran the dental practice.

For example, some add-backs may be reasonable: one-time legal fees, unusual repairs, or certain owner-specific expenses that will not continue. Others deserve a closer look. If the seller added back a family member’s salary, will that role still need to be filled after closing? If continuing education, travel, or auto expenses are removed, are they truly personal, or are they part of how the seller generated referrals and maintained production?

Dental provider compensation is another big issue. If the seller has been paying themselves below market, SDE may look stronger than the practice’s true economics. If you need to hire an associate, retain the seller temporarily, or reduce clinical hours during the transition, the cash flow available for debt service may be different from the adjusted number shown in the package.

For SBA-financed dental acquisitions, lenders generally want to understand whether adjusted cash flow is supportable, repeatable, and sufficient to cover repayment. That means SDE should not just be accepted as a headline figure. It should be tested against tax returns, profit and loss statements, payroll records, production reports, and the buyer’s post-close operating plan.

The question is not simply, “What is the SDE?” It is, “How much of this cash flow is real, transferable, and still available after I pay myself, staff the practice properly, fund working capital, and service the loan?”

3. Purchase Price Multiple

Dental practices are often valued based on a multiple of earnings, a percentage of collections, or a combination of valuation methods. The multiple depends on the practice’s location, size, profitability, payer mix, provider dependency, growth trends, and transition risk.

A lower purchase price is not always a better deal if the practice has declining revenue, outdated systems, or weak patient retention. A higher price may be reasonable if the practice has strong earnings, efficient operations, associate support, and room for growth.

The key is not simply the multiple. The key is whether the practice’s cash flow supports the purchase price, buyer compensation, working capital needs, and proposed financing structure.

4. Debt Service Coverage

Debt service coverage measures whether the dental practice generates enough cash flow to support the proposed loan payments. SBA lenders typically review cash flow carefully, especially in acquisition transactions where the buyer is relying on the practice’s future performance.

A common way to think about this is:

Dental practice cash flow should exceed required loan payments by a comfortable margin.

That margin matters because ownership rarely goes exactly according to plan. Equipment may need replacement. Staff wages may increase. Insurance reimbursement can shift. A buyer may need extra marketing, technology upgrades, or transition support.

Debt service coverage is one reason experienced SBA lenders spend time structuring the transaction, not just quoting a loan amount.

5. Active Patient Count

An active patient count can tell you whether revenue is supported by a healthy patient base or overly dependent on a smaller number of high-value patients.

Ask how the seller defines an “active patient.” Some dental practices count anyone seen in the last 18 months, while others use 24 months or longer. The definition matters.

You will also want to understand how many patients are hygiene patients, how often they return, and whether recall systems are current. A practice with strong hygiene retention may offer more predictable future revenue than one relying heavily on one-time restorative or specialty procedures.

From an SBA lending perspective, active patient count helps support the story behind the cash flow: lenders are not just looking at past revenue, but whether the practice has a repeatable patient base that can reasonably support repayment after the ownership transition.

6. New Patient Flow

New patient flow helps indicate whether the dental practice is still growing or primarily relying on an existing patient base.

Review the number of new patients per month, how they are acquired, and whether marketing costs are sustainable. A practice with steady referrals and strong local reputation may have different risk characteristics than one dependent on paid ads or a seller’s personal network.

For buyers, the question is not just “How many new patients?” It is also “Will those patients keep coming after the ownership transition?”

This is especially important if the seller has been the face of the practice for many years.

7. Provider Production

Provider production shows how much revenue is generated by the seller, associates, hygienists, and other clinical providers.

This number helps identify transition risks. If most production comes directly from the selling dentist, the buyer needs to understand how patient relationships will transfer. If an associate produces a meaningful share of revenue, the buyer should review that associate’s employment terms, compensation, retention risk, and role after closing.

Provider production can also reveal growth opportunities. For example, there may be capacity to add procedures, expand hygiene, improve scheduling, or increase clinical days, depending on the buyer’s experience and the practice market.

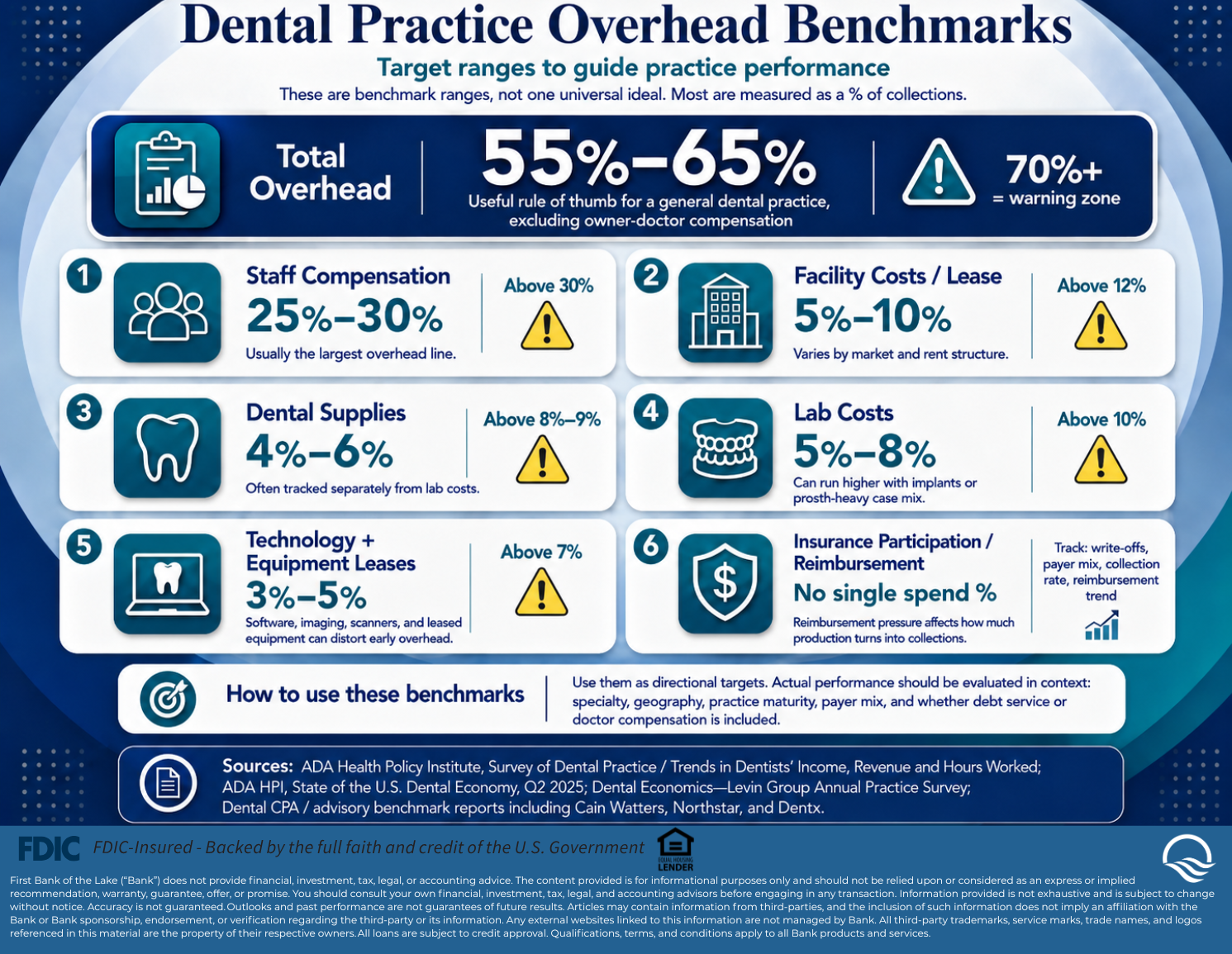

8. Overhead Percentage

Dental practices often have several major expense categories: staff compensation, lab fees, supplies, rent, marketing, insurance, technology, and administrative costs.

The overhead percentage shows how much of revenue is consumed by operating expenses. A practice with strong revenue but unusually high overhead may have less cash flow than expected.

Some expenses may change after the acquisition. The buyer may have different compensation needs, benefits costs, software preferences, or clinical supply habits. That is why historical overhead is useful, but projected overhead matters too.

9. Accounts Receivable

Accounts receivable can reveal a lot about billing discipline and collection quality.

Review total accounts receivable, aging by category, and how much is older than 90 days. A large AR balance may not be fully collectible. If receivables are included in the sale, the purchase agreement should be clear about what is being transferred, how it is valued, and who is responsible for collecting it.

For dental practices with significant insurance billing, AR quality may also reflect coding, claims submission, follow-up processes, and payer mix.

A strong collections process supports cash flow. A weak one can create pressure immediately after closing.

10. Working Capital Needs

Working capital is the money needed to operate the practice after the acquisition closes. It may cover payroll, supplies, rent, insurance, lab bills, marketing, transition costs, and timing gaps between providing services and collecting revenue.

This number is easy to underestimate.

Even if the practice is profitable, the buyer may need liquidity during the transition period. Staff may need reassurance. Patients may need communication. Systems may need updates. Revenue may dip temporarily as ownership changes.

SBA 7(a) financing can often include working capital as part of the overall loan structure, depending on the transaction and lender underwriting. The right amount depends on the practice’s cash cycle, buyer liquidity, and transition plan.

How SBA Financing Can Fit a Dental Practice Acquisition

SBA 7(a) loans are commonly used for business acquisitions, including professional practices such as dental offices. Depending on the deal, proceeds may be used for the practice purchase, goodwill, equipment, working capital, and eligible closing costs.

If real estate is part of the transaction, SBA financing may also be considered for owner-occupied commercial property. SBA 504 financing may be relevant in certain eligible owner-occupied real estate-heavy transactions, while SBA 7(a) is often used when the acquisition includes significant goodwill or multiple financing needs.

Equity injection starts at 10% for certain SBA acquisition transactions, but it can be higher depending on the borrower, project, collateral, seller financing, buyer experience, and overall risk profile. All financing is subject to SBA requirements and lender underwriting.

Why Lender Experience Matters

Dental practice acquisitions are not just generic small business loans. They involve practice valuation, transition risk, seller involvement, patient retention, equipment considerations, real estate or lease terms, and professional licensing requirements.

An experienced SBA lender can help evaluate whether the financing structure fits the transaction. That does not replace your CPA, attorney, practice broker, or valuation advisor, but it can help you understand how the deal may be viewed from a lending standpoint.

First Bank of the Lake is a nationwide SBA Preferred Lender with deep SBA lending experience, including acquisition, franchise, commercial real estate, construction, and other complex transactions. The bank’s role is to help borrowers navigate structure, documentation, expectations, and process with clarity.

With these 10 numbers in hand, you are in a stronger position to look past the asking price and evaluate whether a dental practice truly fits your goals, your financing needs, and your long-term ownership plans.

FAQ: Buying a Dental Practice with SBA Financing

Can SBA financing be used to buy a dental practice?

SBA 7(a) is often the more flexible option. In dental lending, it is frequently used for practice acquisitions, working capital, partner buyouts, ownership changes, certain refinances, or projects with several uses of funds.

How much down payment is needed to buy a dental practice with an SBA loan?

Equity injection starts at 10% for many SBA acquisition transactions, but it can be higher depending on the buyer, transaction, seller financing, collateral, and lender’s credit analysis.

Can SBA financing include working capital?

In many cases, yes. SBA 7(a) financing may include working capital when it is properly supported and part of an eligible loan structure.

Can SBA loans finance dental office real estate?

SBA financing may be used for eligible owner-occupied commercial real estate, subject to SBA program requirements. Investment or primarily tenant-leased properties are typically not eligible.

What is the most important number when buying a dental practice?

No single number tells the full story. Seller’s Discretionary Earnings, debt service coverage, revenue trends, active patient count, and working capital needs should all be reviewed together.

First Bank of the Lake (“Bank”) does not provide financial, investment, tax, legal, or accounting advice. The content provided is for informational purposes only and should not be relied upon or considered as an express or implied recommendation, warranty, guarantee, offer, or promise. You should consult your own financial, investment, tax, legal, and accounting advisors before engaging in any transaction. Information provided is not exhaustive and is subject to change without notice. Accuracy is not guaranteed. Outlooks and past performance are not guarantees of future results. Articles may contain information from third-parties, and the inclusion of such information does not imply an affiliation with the Bank or Bank sponsorship, endorsement, or verification regarding the third-party or its information. Any external websites linked to this information are not managed by Bank. All third-party trademarks, service marks, trade names, and logos referenced in this material are the property of their respective owners. All loans are subject to credit approval. Qualifications, terms, and conditions apply to all Bank products and services.